What Should Allowance Actually Teach Your Kid in 2026?

Cash App now offers managed accounts for kids as young as 6, and fresh data from 9,000+ families shows what parents really pay. The amount is the least interesting part. Here is how to design an allowance that works as your kid's first money system.

Why is allowance suddenly a tech product?

Allowance used to be a five-dollar bill on the counter. In 2026 it's a product category. Cash App, which already serves more than 5 million teens monthly, rolled out managed accounts this spring for kids as young as 6, complete with automated transfers, parent controls, a kid-designed debit card, and spending insights. Apps like Greenlight, BusyKid, Acorns Early, and Till compete for the same job: moving family money to smaller family members.

The fintech industry has decided your eight-year-old is a market. Which means parents are now making a design decision whether they realize it or not: what is this weekly transfer supposed to teach?

Allowance is your kid's first money system, the place they form default beliefs about earning, spending, and waiting. The dollar amount matters less than the design. Get the design right and a few dollars a week quietly builds the instincts everything else depends on.

How much are families actually paying in 2026?

Till Financial published a useful data set this spring covering 9,135 U.S. families. The average weekly allowance was $17, but the median was $10, meaning a small group of high-paying families drags the average up.

By age, the ranges run roughly like this: $7 to $10 a week at age 10, $10 to $15 at 12, $12 to $18 at 13, $18 to $25 at 15, and $20 to $35 at 16, with the biggest jump landing between 13 and 15, right when kids start buying food with friends and shopping online.

Hold the numbers loosely, though. The right amount depends on what the money has to cover. Ten dollars that has to stretch across snacks, games, and gifts teaches budgeting; ten dollars of pure fun money on top of parent-paid everything teaches nothing except that money appears. Decide what your kid is now responsible for buying, then size the allowance to make that job possible but snug.

Should allowance be tied to chores? The honest debate

Both camps in this old fight have a point.

The pay-for-chores camp says kids should learn that money comes from work. The no-strings camp counters that chores are family citizenship, not a job, and that paying for them teaches kids to negotiate a rate for making their own bed. Both are right, which is why the hybrid keeps winning in practice.

The hybrid: a base allowance that isn't tied to chores, because dishes and decent behavior are what humans in a household do for free. Then, separately, paid work: bigger, optional jobs beyond the baseline. Washing the car, clearing the garage. Posted rate, claim it or don't.

This split teaches two different truths at once. Baseline: you contribute because you belong. Paid tier: extra money exists, and it comes from noticing work and doing it well. Kids who grow up with the second tier tend to be the ones who, at twelve, start noticing the neighbors' cars are dirty too. That's the seed of everything.

Weekly or monthly? The feedback loop question

In Till's data, 72% of parents pay weekly, and for younger kids that's the right call for a reason worth understanding: feedback loops.

A seven-year-old's sense of time is short. A week between payday and payday means a week between decision and consequence: blow Saturday's money on slime by Sunday, and the lesson arrives while the memory of the slime is still fresh.

Teenagers are the opposite case. Somewhere around 14 to 16, switching to monthly is a quiet upgrade, because a month is long enough to require actual planning. Running dry on day nine and sitting with it until the first is a low-stakes rehearsal for every paycheck they'll ever manage. Better to fumble a $90 month at fifteen than a $3,000 month at twenty-three.

Simple rule: pay young kids fast enough that consequences connect, and pay teens slow enough that planning is required.

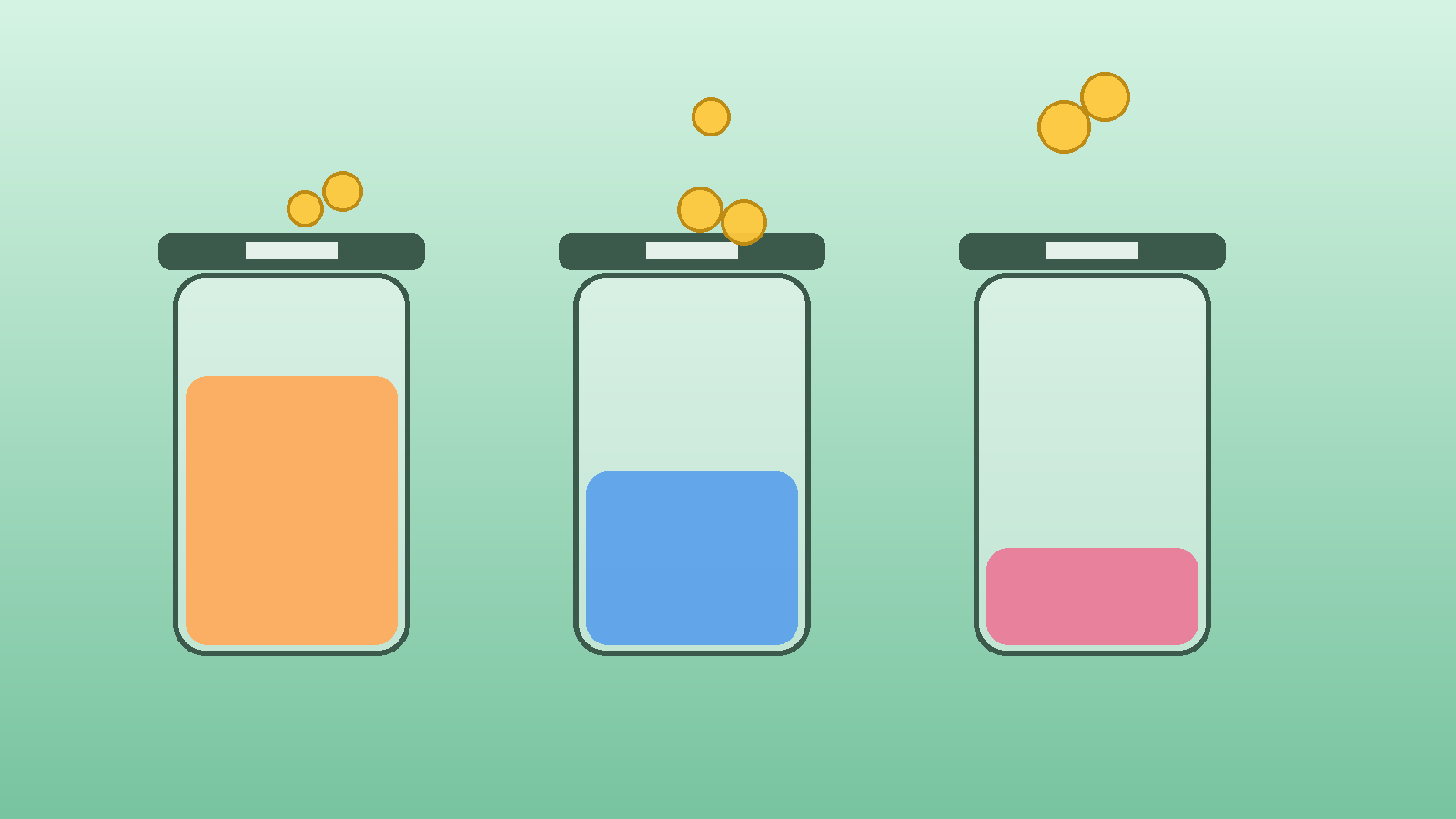

Does the three-jar split still work in a cashless world?

The classic advice was three jars: spend, save, give. The jars became app buckets, but the split matters more than ever precisely because digital money is invisible. A kid can see jars filling; a balance on a parent's phone is just a number that sometimes says no.

Whatever tool you use, recreate the buckets and let your kid set the ratio inside guardrails. Spend is the everyday money, and it should be allowed to be "wasted" on things you find silly, because low-stakes regret is the entire pedagogy. Save is for a named goal with a picture: "savings" is a chore, "the bike fund" is a countdown. Give is small but real, chosen by the kid, because deciding what deserves your money is a values workout.

Families with older kids sometimes add a fourth bucket: invest or grow. Even a few dollars flowing there monthly opens the compounding conversation early.

Apps versus cash: what does each actually teach?

Parents keep asking which app is best. Wrong first question. The first question is what cash teaches that apps can't, and the reverse.

Cash teaches scarcity you can feel. A ten-year-old holding three dollars after spending seven understands subtraction in their body. App reviewers keep landing on the same caution: frictionless digital spending can hide the loss moment that makes young kids actually learn. For ages 6 to 9, there's a strong case for physical cash.

Apps teach the world kids will actually live in: card payments, transfers, autopay, checking a balance before wanting things. From about age 10 up, that fluency matters, and the good apps add chore boards, goal trackers, and parental visibility cash can't match.

So sequence it instead of choosing: cash first for the feel of money, app second for the mechanics of money. And when the app arrives, keep the weekly conversation; parent surveys are blunt that the talk, not the tool, is what predicts financially confident kids.

When does allowance become seed capital?

Here's the upgrade most families never make: somewhere around age 9 to 12, allowance can stop being only income and start being capital.

It begins the first time your kid wants something bigger than their savings bucket and asks for more allowance. The default parent moves are "no" or a raise. The interesting third move: "your allowance is what it is, but there's no cap on what you can earn." Then help them see the paid-work tier and, beyond it, the first real business question: what could you make or do that someone would pay for?

A surprising number of kid businesses are funded exactly this way: four weeks of saved allowance buying the first bag of loom bands or lemonade supplies. The allowance was the seed round, and the kid learns the most important money sentence there is: money can be spent, saved, or put to work.

Foundra Kids has simple planning templates that turn "I want to sell bracelets" into a one-page plan a nine-year-old can actually follow: what it costs, what to charge, who buys.

Why the conversation beats the transfer

One finding shows up in essentially every study of youth financial literacy, including this year's family banking research: parent-led money conversations are the single biggest predictor of teen financial confidence. Not the app. Not the amount. The talk.

The talk is free. But automated allowance quietly deletes it. When the transfer fires silently every Friday, the weekly moment where money changed hands disappears into a notification nobody reads.

So if you automate, and automation is fine, deliberately rebuild the moment. A ten-minute Sunday check-in does it: what came in, what went out, how's the bike fund, any regrets? "The slime was gone in a day, huh" delivered with a grin beats a lecture.

And narrate your own money life out loud. "I'm waiting for these shoes to go on sale." "We're skipping takeout this week because the car needed brakes." Kids assemble their money worldview from overheard sentences. Give them good ones to overhear.

The ladder: allowance, earnings, first business

Zoom out and allowance is rung one of a ladder you climb over a decade.

Rung one, ages 6 to 9: base allowance, cash, three buckets, weekly rhythm. The skill is choosing and waiting. Rung two, ages 9 to 12: the paid-work tier appears, an app can enter, the save bucket gets goals with names. The skill is connecting effort to money. Rung three, ages 11 to 14: first outside earnings (pet sitting, lawn edges, a market-day table) and maybe allowance-as-seed-capital. The skill is noticing that strangers will pay for value. Rung four, 14 and up: monthly pay cycle, a real bank account with a debit card, a slice of real responsibility like their own clothing budget, and for some kids, an actual small business with books.

Each rung keeps the same weekly conversation, just with bigger numbers, and each is allowed to wobble.

Parents who climb this ladder send eighteen-year-olds into the world who have already run out of money a dozen times, at stakes that never mattered. That's the whole game.

Frequently asked questions

What's the average allowance in 2026? Across 9,000+ families on one major platform, the average is $17 a week but the median is $10, and $10 is the more honest benchmark. Age and responsibilities should move the number more than averages do.

Should I stop allowance when my teen gets a job? Don't stop it abruptly; renegotiate it. Many families shift the allowance toward covering fixed responsibilities (clothing, gas share) while the job funds wants.

Are kid debit cards safe? The major kid banking apps are FDIC-insured through partner banks and give parents controls and visibility. The bigger risk isn't safety, it's invisibility: pair any card with a regular money conversation.

My kid blows every dollar instantly. Do I intervene? Protect the save bucket mechanically (it transfers before they touch anything) but let the spend bucket be theirs to torch. The regret is the lesson; your job is keeping regret affordable.

Is 6 too young to start? Cash App's new accounts start at 6, but readiness is about counting, not birthdays. If a kid can count coins and wait a week, they're ready for a small start.

Sources

Ready to help a young entrepreneur get started?

Foundra Kids gives young founders a simple, fun way to plan their first business.

Try Foundra Kids